Today’s first problem: how does automobile usage increase with GDP? We expect that, as people grow wealthier, their use of automobiles increases. I managed to find a great paper detailing that relationship:

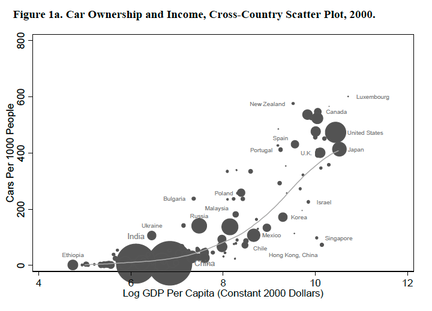

(The graph is mislabeled: “Log” should be “ln”) Now all I have to do is reduce this to a simple algebraic form. A rough straight line runs from the word “China” through Luxembourg, characterized as y=180*(ln(GDP/capita) -7.5) for values of GDP/capita > 7.5. The problem with this is that I can’t afford to saddle my players with natural logarithms. So I have to convert that to linear form, requiring even poorer approximation: total cars = population * (GDP/population - 5000) / 40,000. Moreover, this doesn’t take into account income inequality — the same problem that bedeviled me with malnutrition (there are enough calories produced to feed everybody, but millions die of malnutrition while others suffer from obesity).

Worse, this covers only automobile ownership, not automobile usage. I need to know how many miles those cars are driven. Perhaps I can sidestep all this by treating it as an energy problem rather than an automobile problem. That is, calculate gasoline use instead of automobile mileage. This renders my energy calculations more complex. Right now, I assume that all energy use is interchangeable: an exajoule of electricity is no different from an exajoule’s worth of gasoline. This, however, is a pretty gross approximation; perhaps it would be better to break out energy by usage type: transportation, electricity, and heating are the three biggies.

Another question: should I permit taxation of automobiles explicitly? Or perhaps taxation of gasoline? Sheesh, this is getting messy.

July 1st, 2:00 PM

Today I’m struggling with the calculation of energy usage (again). It turns out that there’s no solution to the basic problem, which is to create a standard formula for calculating the supply of each form of energy given that:

1. The current price of each form is $30 billion per exajoule. (assumption of a stable market)

2. The long-term supply is in some wise congruent with the numbers for proven reserves.

3. A 1% increase in price, should, for the short term, lead to a 1% increase in supply for all forms.

There’s no formula that fits these boundary conditions, because the market is not truly stable. So what should I do?